BTC index: April 2021

A close look at the Russian ruble as new sanctions bite

Unusually quiet

This was a relatively low volatility month in terms of the premium/discount paid for bitcoins relative to the official USD exchange rate across a large proportion of countries tracked by the btc index. Usually the discount or premium can jump around wildly, especially in countries with low exchange volume. For some reason, the past month saw a drop in this kind of volatility - though it was far from a quiet month.

This month’s spotlight turns on the Russian ruble, which saw a spike in the volume exchanged and premium paid for bitcoins as newly economic sanctions were imposed. The Russian Federation is an interesting case study for bitcoin adoption and use given a few unique macroeconomic trends including as its monetary policy, the falling tendency to use USD in international trade and the desire to develop an alternative payment networks to SWIFT.

A quick note on the Venezuelan Bolívar

For the first time in many months the Bolívar is not #1 in terms of movement of index value. This is because, for some reason, the foreign exchange rate feed suddenly begun reporting a VES/USD exchange rate that reflects something closer the correct exchange rate (i.e. instead of ~9.8 to 1 USD it is closer to ~2.8m to 1 USD. I’ll have to chase up why this is the case but this is more consistent with the implied rate that one derives using the btc index of ~2.1m to 1 USD. If the new feed is correct, and reporting from the ground suggests that it is not, then the VEF/VES trades at a discount in BTC/USD terms.

Top 5 movers for the month

Ugandan shilling (+0.48)

Namibian dollar (-0.37)

Botswanan pula (+0.17)

Eritrean birr (+0.16)

Omani rial (+0.15)

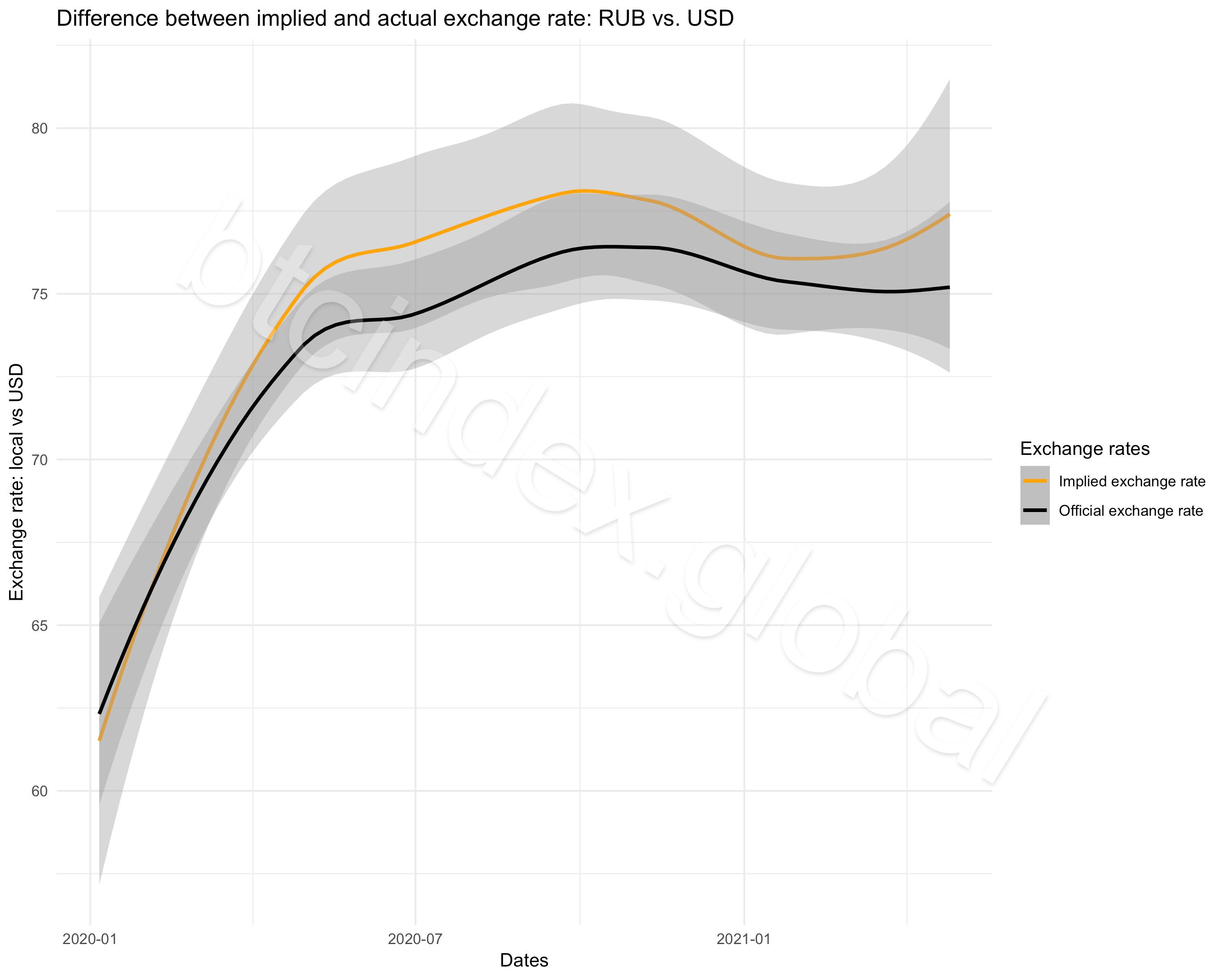

Spotlight: Russian ruble

The imposition of economic sanctions on a country has the consequence of increasing demand for and use of alternate payments networks, like bitcoin, which over time blunts the effectiveness of said sanctions. A closer examination of the Russian Federation through the btc index lends some support to this statement. Moreover, bitcoin can be placed within a larger set of macroeconomic trends related to a drive for greater economic self-sufficiency such as tightening of monetary policy, decreasing reliance on the US dollar as a medium for settling international trade and development of alternatives to SWIFT.

Economic sanctions as a driver of bitcoin use/price

Numerous rounds of economic sanctions have been imposed on individuals or companies in the Russian Federation over the last decade. Some of the most punitive came from the US and EU in 2015 following the Russian Federation’s annexation of Crimea. In April 2021 additional sanctions were levied to bar, “U.S. financial institutions from trading new debt issued by the Russian central bank, Finance Ministry and sovereign wealth fund” (h/t Bloomberg).

In the aftermath the RUB/USD exchange rate fell a bit under 2% (h/t source). It is at this point that the premium paid for bitcoins in rubles, converted to USD terms, spiked going from a difference of +1.9% to -9%. The volume of bitcoins exchanged peer-to-peer in the Russian Federation has also increased 4x since January 2021.

It is worth considering that on the day that the ‘ruble crashed’ the ~2% drop relative to the dollar is nothing when compared to the drop from 60 to 73 rubles per USD during the first half of 2020. Notice also how tightly bitcoins sell to their official USD exchange rate terms during this period. Notice too the point at which this tight coupling becomes a premium and how persistent that premium has been since. People want bitcoins in the Russian Federation and there are good reasons why so.

If economics sanctions are a driver of the adoption and use of bitcoin, heavier and heavier sanctions eventually work against themselves in that they result in a greater need to develop and use alternate economic systems so as to mitigate the effects of the sanctions. Over time, the power of the sanctions wane as they become less effective in the face of the new systems like bitcoin. Looking around at other countries in the world where economic sanctions are most numerous and strongest (e.g. Iran, North Korea) - suggest that this trend is not limited to the Russian Federation. This will be a topic revisited in future issues of the btc index.

Capital flight and macroeconomic policy

The picture is a little less clear when attempting to assess the prevalence of capital flight in Russia and what role bitcoin might play in it.

An interesting feature of Russian macroeconomic policy, relative to other parts of the world, is that interest rates are allowed to rise. This should help stem the tendency toward capital flight. The most recent move resulted in an increase of 50 basis points to 5%. This represents a counter-weight, in the form of a stronger incentive to keep capital ‘at home’ and reduced need for alternative savings vehicles, to the increased demand for bitcoin as a consequence of economic sanctions.

By contrast, if one examines the in and out flows of bitcoins to exchanges using the very handy Crystal tool, a slight different picture emerges. During 2020 there was a net outflow of bitcoins from Russia of ~US$20m equivalent (US$82m outflow vs US$66m inflow). Most of these outflows were to the Seychelles. Contrast this with the first quarter of 2021 where there was ~US$60m outflow (US$64m outflow vs US$4m inflow). Most of this outflow left from the local Buy Bitcoin Pro exchange. If this trend continues then 2021 is set to be a year with the largest outflows of bitcoin from Russia ever. With sanctions biting, and more possibly to follow, how will this trend play out?

The drive for an alternate global payments network

Partly as a consequence of economic sanctions, and to counter the threat of potential future economic sanctions, for many years the Russian Federation has attempted to reduce its reliance on the Society for Worldwide Interbank Financial Telecommunications (SWIFT) network. SWIFT is a messaging network that financial institutions use to securely transmit information and instructions through a standardized system of codes. It is one of the key ‘plumbing’ networks in the world financial system.

The Russian Federation’s most direct attempt to reduce reliance on SWIFT took the form of an alternate, but interoperable, payments communication system called Mir. While Mir has not yet lived up to its stated goals, the desire to reduce the risk posed by restricted SWIFT access through an alternate payments system was restated recently by the Defense Ministry spokesperson Maria Zakharova.

It is worth considering that the need to develop an alternative system, like Mir, when there are now decentralized systems whose access cannot be cut off due to their very technical design. In terms of peer-to-peer bitcoin trading, the sheer volume conducted in the Russian Federation eclipses that seen in other countries covered as part of the btc index. This suggests that, absent any kind of overarching and top-down payments system like Mir, people are just going to go with whatever is available thereby creating this change from the bottom-up.

To close, it has become clear that the Russian Federation has been reducing its payments to trade partners in US dollar, preferring instead to settle in Rubles or Euros (h/t Adam Tooze). An interesting thought experiment would consider what proportion of this trade might be settled using bitcoin, or some other payment mechanism, and what the consequences of this shift might entail?

Regional charts

Currencies/countries to look closely at this month include:

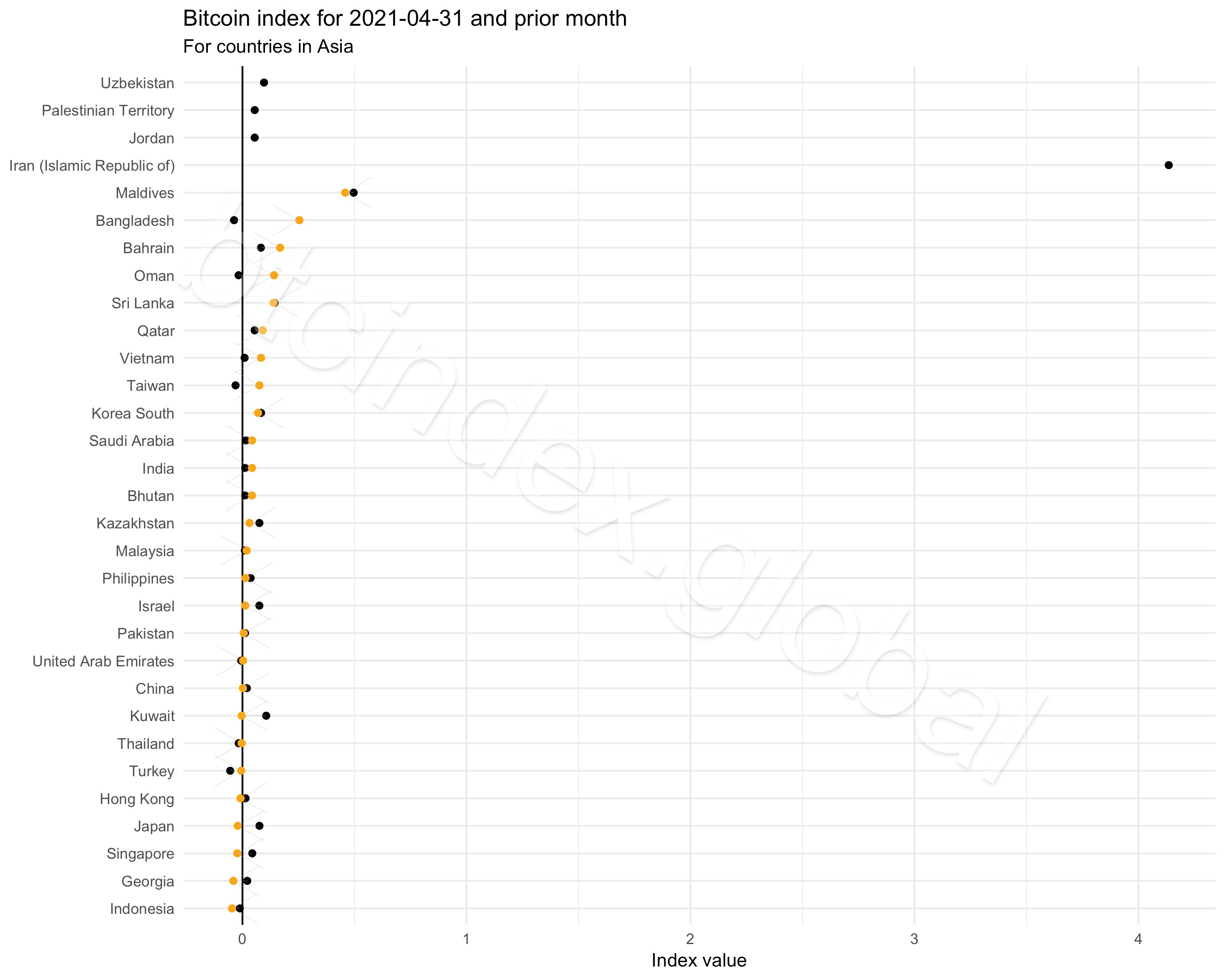

The Bangladeshi taka’s premium for bitcoins rose the most out of the countries in Asia. This came amid a spike in volume of btc purchased in taka during the month. It also marks an inflection point where the taka has stopped trading at a slight discount in bitcoin terms.

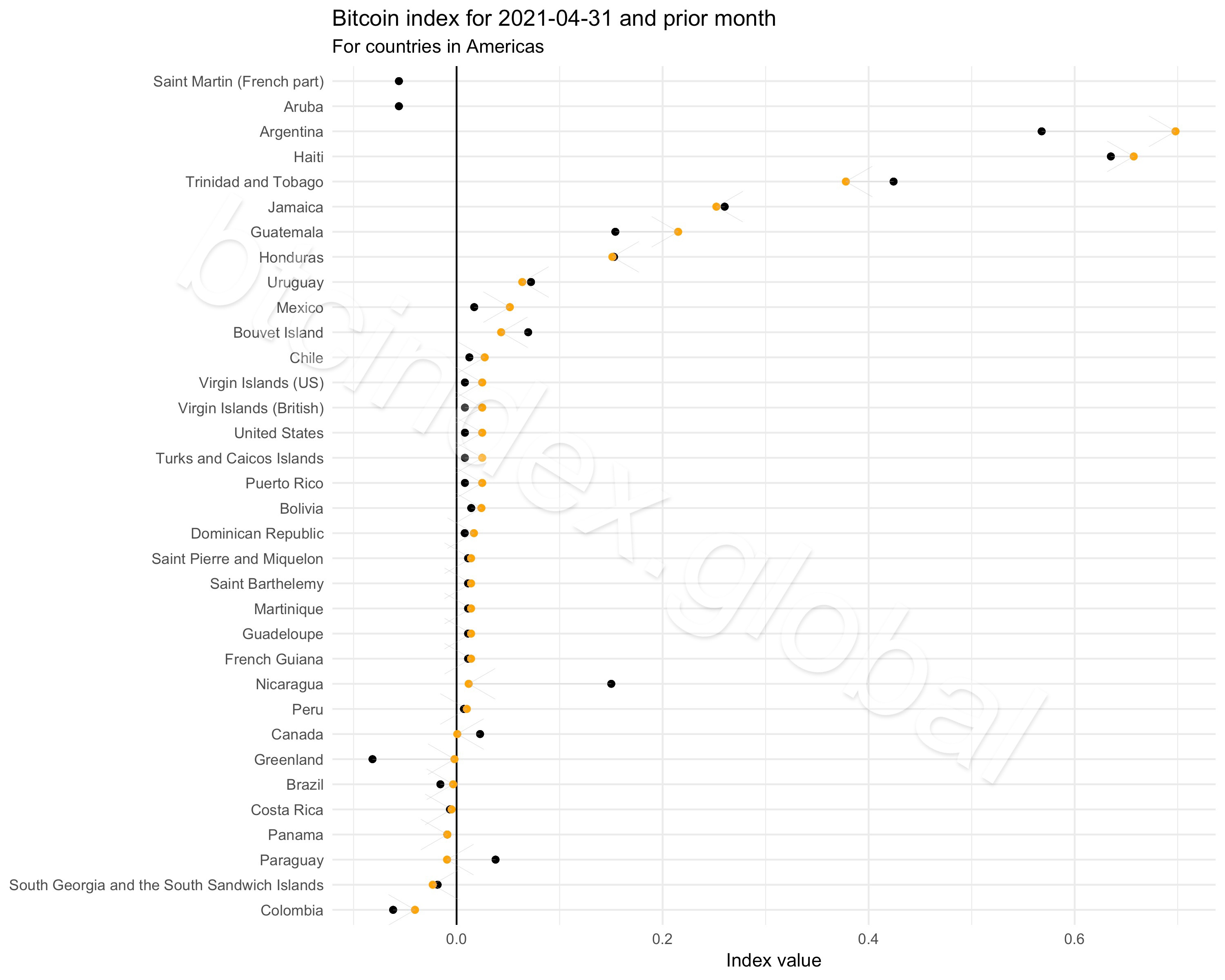

The premium on the Argentinian peso continued to rise, a bad sign for the country’s macroeconomic state, while the discount on the Colombian peso retreated slightly.

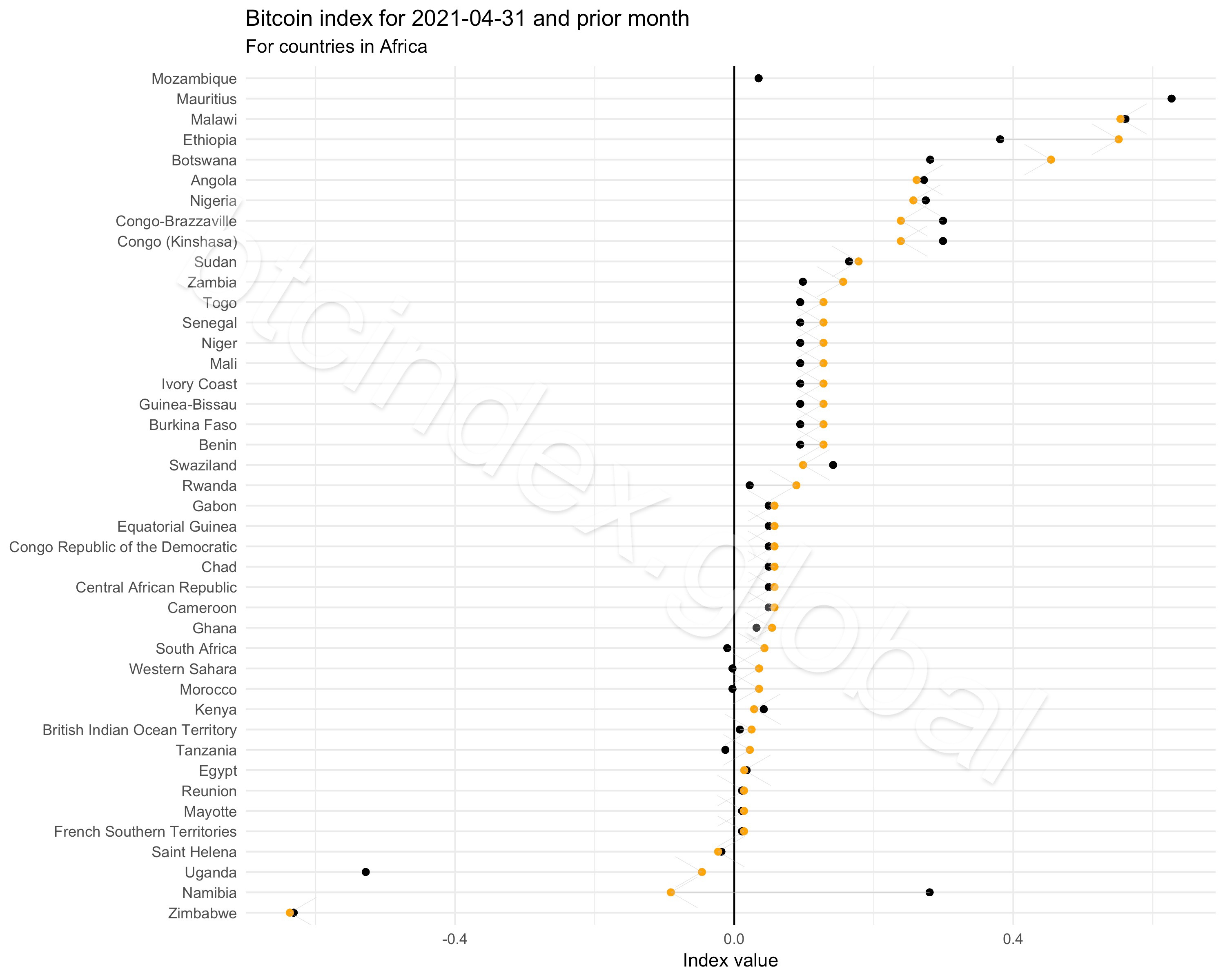

The Ethiopian birr continues to trade at a relatively stable premium in the face of a depreciating official exchange rate.

The Hungarian forint has moved into position #1 in terms of bitcoins selling at a discount relative to the official HUF/USD exchange rate in Europe.

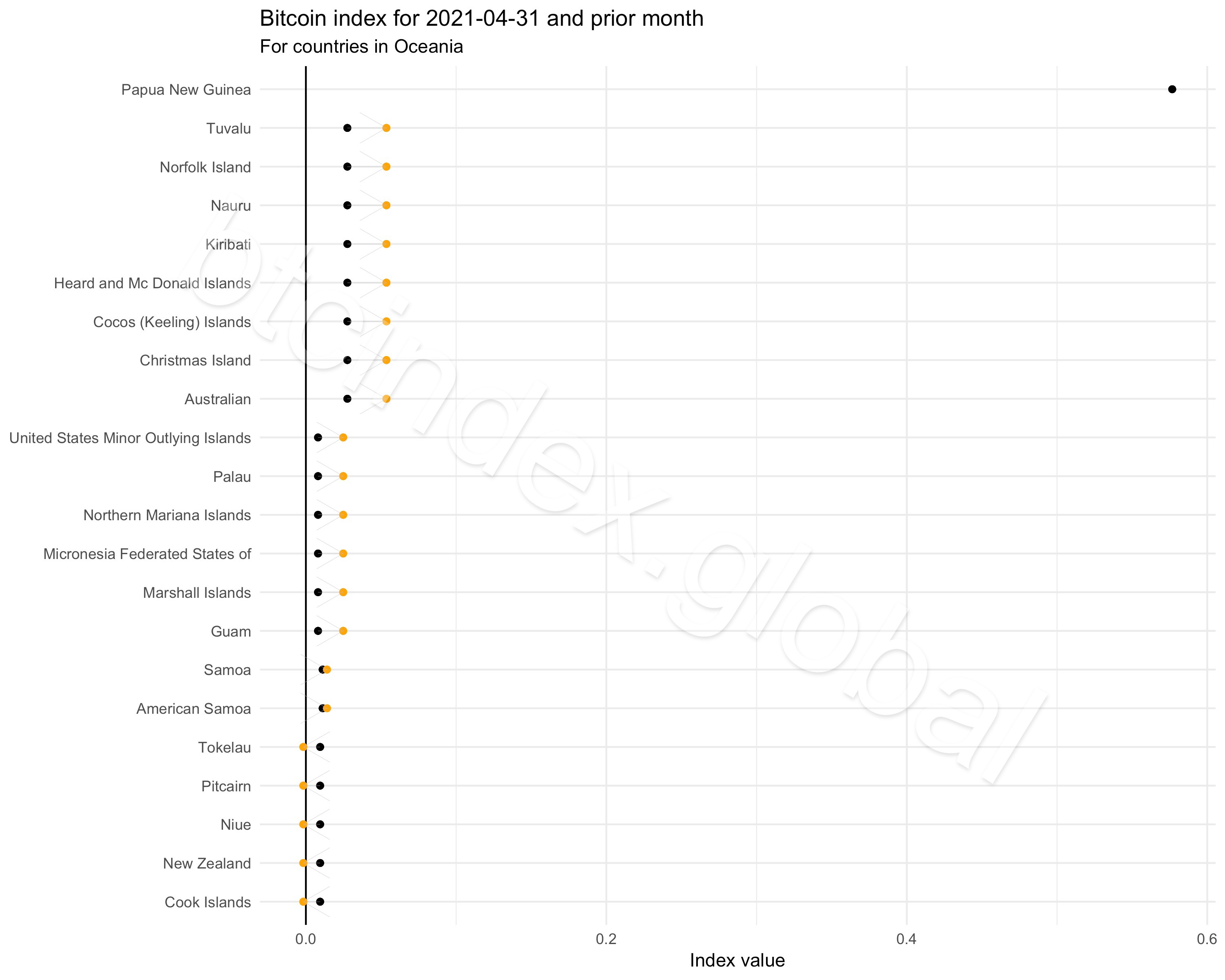

A very small amount of Papua New Guinean kina is exchanged for bitcoins some months. Nevertheless, when it does trade it does so at a stable rate of +100% relative to what it should trade at in official USD terms.

Asia

Americas

Africa

Europe

Oceania

Past months

March 2021 - Turkey

January - February 2021 - Lebanon

Subscribe for auto-updates…

That’s it for this first monthly bulletin of the btc index. Each month a new bulletin will be posted with insights about why deviations and changes are seen across countries and currencies.